Protection against the storm

Written by Pablo González and Pedro Nonay, trying to find what we can do in our adaptation to changes in world order.

Entry 3

Currencies.

September 18, 2024

As I announced in the previous entry, I will now begin to deal individually with each change that we are going to face. I will also try to present the alternatives for action to protect ourselves.

I already said in that entry that I will not order these changes in order of importance, but based on the urgency we have to adapt. In other words, I will first deal with what, in my opinion, is needed first.

For this reason, and since economics affects almost everything, I will begin by addressing the issue of currencies.

I know that the economy is much more than currencies (I will deal with those other issues later), but we use currencies to measure everything economic. And, … I think that’s a big mistake today.

Chewing gum.

To measure lengths, we use the meter. Let’s think about the construction of a house. Let’s imagine that the plumber, to measure the length of a pipe, comes with an elastic meter (stretchable and shrinkable). I think it is obvious that no one would rely on his measurements to make decisions on the construction site. They would ask him to use a more “serious” meter.

Well, … exactly that is what is happening with currencies. With inflation, the measures are elastic. The reality is worse, because what we call inflation is better defined as loss of currency value.

However, we continue to use currencies to measure everything economic. In other words, we have a false blueprint with which we make decisions. Not infrequently, the results are not good.

When we want to get a little more professional, we talk about “constant prices” (big fallacy). We do this by updating yesterday’s prices with inflation measured by the CPI. It wouldn’t be bad if there were the double circumstance that all things had the same CPI (something that never happens), and that the CPI reflected reality and was not manipulated (something that never happens either). So this apparent solution does not solve any problem.

Things get more complicated when we look for exchange rates between two currencies (for international business), since there are even more artifices. It becomes a three-dimensional chewing gum.

Definition of currency.

In classical economics it is said that, to be considered currency, an asset must have three characteristics:

- It must be a “store of value”. That is, if you keep it, it retains its value.

- And, “unit of account”. That is, it can be used to measure the economy and make value comparisons.

- And, “means of payment”. That is, they accept it in transactions.

Well, nowadays, the major currencies (dollar and euro), only fulfill the third characteristic, because it is true that they let you pay with euros or dollars almost everywhere.

Let’s look at “store of value”.

The truth is that all currencies lose value over time. It is not only inflation (which also happens). The fact is that coins even disappear. They did, from the Roman denarius to the real de a ocho of the Spanish empire. Of course, so did the German mark of the Weimar Republic, … , and so will the dollar and the euro, at some unknown point in time.

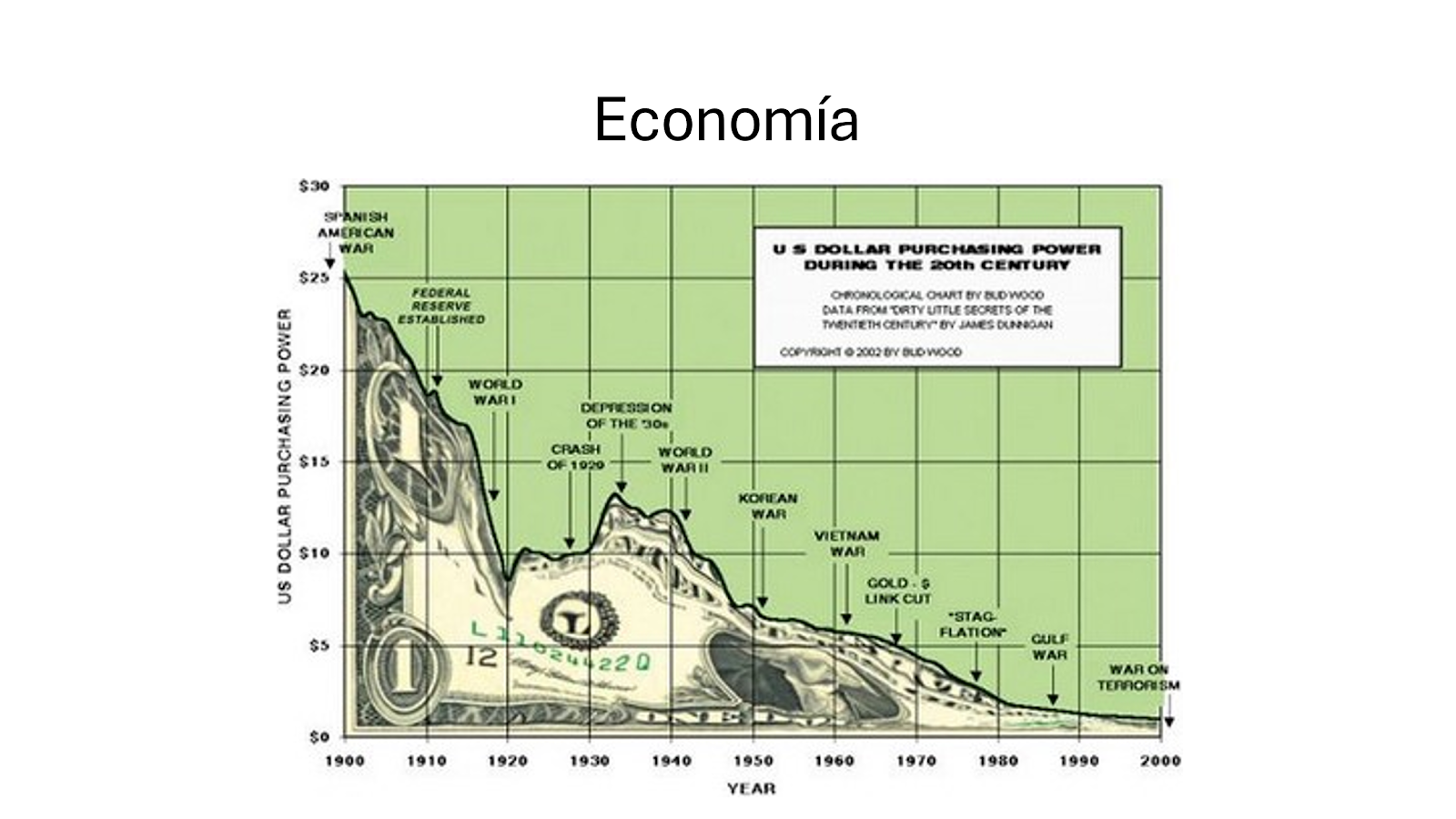

Meanwhile, before disappearing, the dollar has lost most of its value since 1900, as seen in the following chart.

Therefore, if we had kept a dollar in the “piggy bank” in 1900, we could buy, today, 25 times less things with it. This cannot be considered a good “store of value”. It is not the recommended place to “archive our long-term savings”, even if the dollar does not disappear yet.

Unit of account.

It may seem that this concept is almost the same as the previous one, but there are many more implications. Both psychological and legal.

As far as legal requirements are concerned, we are obliged by law to do our accounting and tax returns in the official currency of our country.

As for the psychological ones, we tend to “count” our wealth in that currency. We tend to think: “I have x dollars, so I can do x things”.

But, as the currency is manipulated (and loses value, as we have seen in the previous section), these accounts are false. We may be obliged by law to make our tax returns in that currency, but we should not do our personal accounting in it.

It would be necessary to make what in mathematics is called a “change of coordinates”.

For that, let’s imagine that, instead of measuring our wealth in euros, we measure it in “gold”.

Today we are told that there is a lot of inflation. That everything has gone up in price. They even say that we are in an “everything bubble”.

That is true if we measure things in “dollar coordinates”. But it is not so true if we measure them in “gold coordinates”.

I try to explain it with two examples. The thing is that most people have their wealth “archived”, either in real estate (their house, or other properties), or in stocks, bonds, ETFs, …

To give the example of real estate, as I do not trust manipulated statistics, I am looking for personal data. The fact is that the first house I bought (in 1990), cost me 20 million pesetas, which was about 120,000 €.

I looked at homes for sale today in the same neighborhood. I didn’t find my old house for sale, but I did find a very similar house next door. It is for sale for 625,000 € (and, as it is built in the same period as my old one, it needs renovation, which means more money to spend).

The first conclusion (if we think in “euro coordinates”) is that housing in this neighborhood has multiplied its price by 5.2 times from 1990 to today.

Now let’s think in “gold coordinates”. If, at that time, I had had my savings invested in gold, given that one ounce of gold was worth in 1990 about 380 dollars, and given that one dollar cost, in 1990, 102.02 pesetas, which, converted into euros, is 0.6 €, that means that one ounce of gold cost 228 € in 1990 (approx.).

Therefore, my house would have cost me (in 1990) about 526 ounces of gold.

An ounce of gold is trading today at €2,326. This means that 526 ounces is almost €1,224,200.

Therefore, “measuring in gold”, my house would have had a drop in price (from 1990 to today), from the 1.224.200 € worth today the amount of gold that it cost me to buy it, to the current 625.000 € (plus remodeling works), that they ask today for a similar house. That is, it would have lost almost half of its value. Which is very different from the 5.2 times I said it would have gone up in price if we measured it in euros.

In other words, things change a lot, in terms of price increases, depending on the unit of account we use (euros or gold).

The above is about the example of “filing savings in real estate”. But, I have already said above that the other place most people use to “file savings” is the stock market. Let’s look at that example below.

In the case of the stock market, it is easier to find the data. This is because the stock and gold markets are both listed.

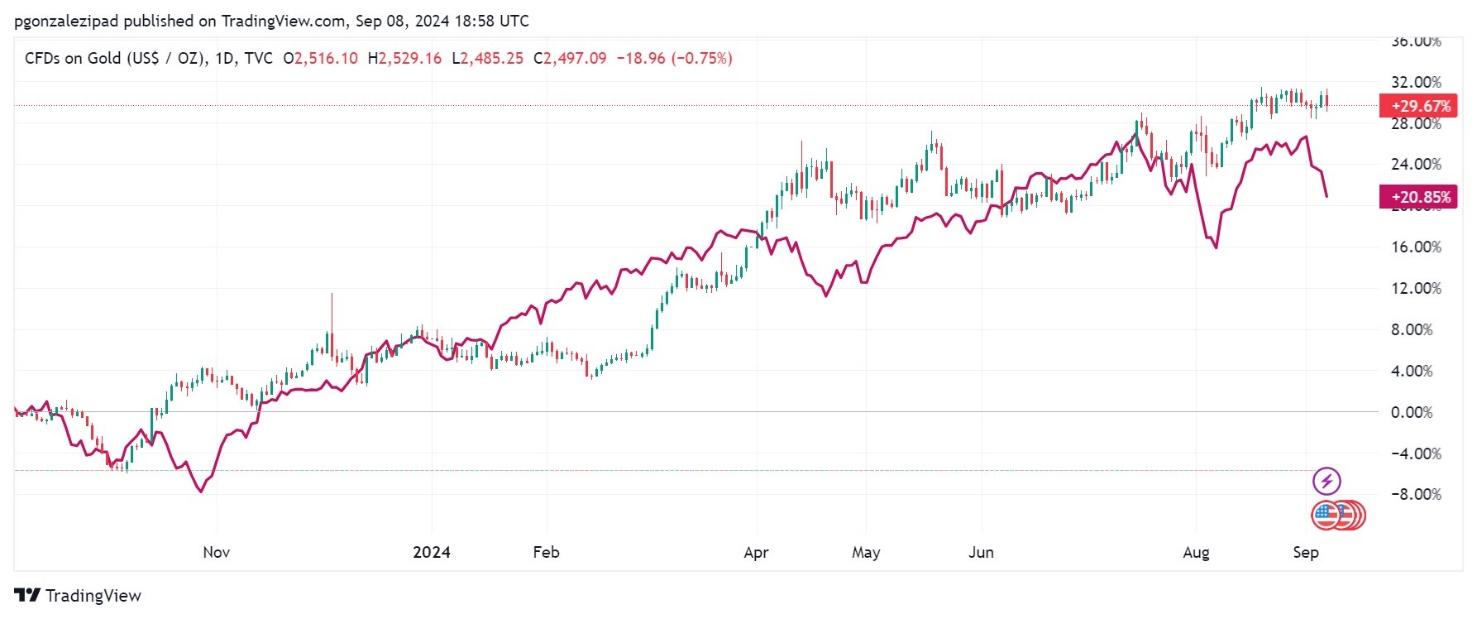

I have found on Tradingview, which is a very respected and useful website, the following chart comparing the share price of the S&P500 (the summary index of the largest US listed companies) with gold.

This chart refers to the last year. The purple line is the price rise of the S&P500, and the green line is the price rise of gold.

The conclusion of the chart is that, in the last year, the stock market has risen less than gold. And this year has been considered a year of great stock market rise (and bubble).

In other words, if we “measure it in gold”, the stock market has gone down this year.

The above leads me to the conclusion that the dollar unit of account is not valid, even if it is the one we use in our accounting (and in our brains).

Given this, the question must be asked: is there one unit of account better than another? The answer is never perfect. However, I wrote some time ago (in this link, in the last point of that entry) how the loss of value of gold has been since the time of Jesus Christ (it was insignificant).

Therefore, gold seems a better long-term “unit of account” than the dollar. At least if we compare it with the stock market or real estate.

The above does not mean that we have to have our savings invested in gold (although it is an option). What I mean is that it deserves that we do the return comparisons of what we have with gold, and not with the dollar. At the very least, it will give us useful information to think about.

Another thing we can do is to choose another unit of account. One that reflects well the “replacement prices” of our main activity. For example, if I were a potato farmer, I would try to compare any price with the price of a kilo of potatoes. I would think: How many kilos of potatoes does it cost me to buy a house, or how many kilos does it cost to buy the tractor I need? If the answers go up in price, I would know that I have a problem, because either I increase my potato production, or I will be able to buy less things.

Since I am not a farmer, but my core business is real estate, I try to measure everything in square meters of the kind I work with. Although I also do it with gold, and even bitcoin.

There are many possible units of account to choose from. Everyone must find the one that best suits his or her activity. For example, we could measure everything in “energy” (the price of KWh, or the price of a barrel of oil), since energy is needed for everything. In fact, something similar is what we used to do with the petrodollar. But we can also think of products of habitual consumption, which are not perishable and whose prices are not too manipulated (salt?).

Currencies and power.

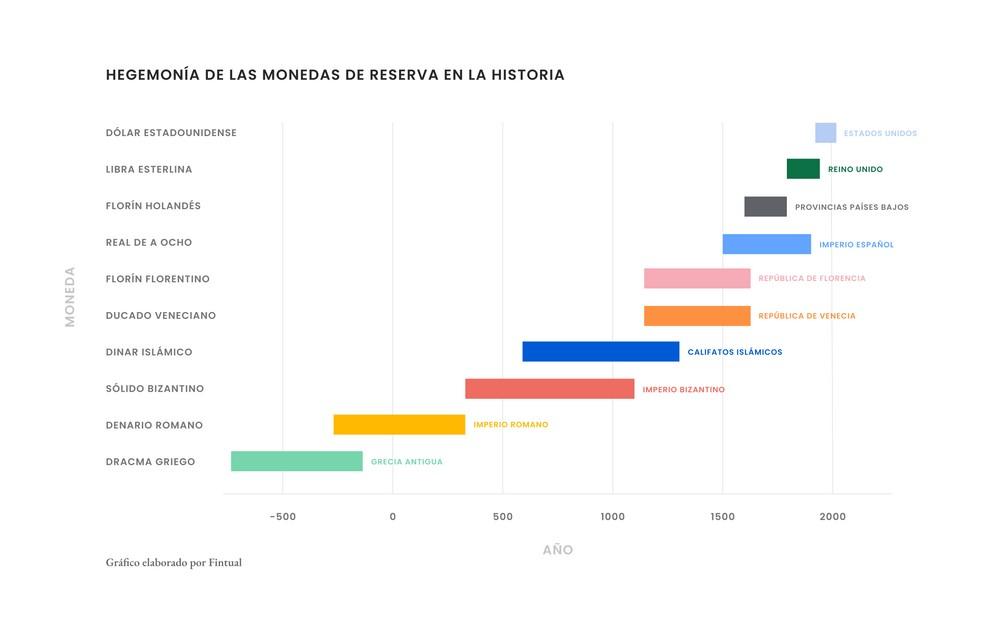

As is logical, currency control has always been closely linked to power. And the control of the hegemonic currency has been linked to the most relevant empire in the world at each historical moment, as can be seen in the following graph (to which some detailed objections can be raised, but it reflects the concept very well).

Source: Fintual

It is interesting to note how, since the Renaissance, the half-life of each hegemonic currency is shorter than in ancient times. Probably for the reason that the printing press makes knowledge flow faster, and that allows competitors to design and implement their alternatives faster. This will accelerate even more after the Internet.

The fact is that all currencies eventually lost their hegemony. So will the dollar. In fact, the above comment that it is becoming a worse and worse “store of value” and “unit of account” is a sign of its decline.

Possible scenarios.

With respect to currency, within a few years it could happen:

- That those who govern achieve what they call a “soft landing”, and that inflation ends. Even so, the accumulated inflation of the previous years would still exist, which according to the official (gimmicked) indexes is something more than 20% since the pandemic.

- They may not succeed, and after a year or two of mirage, inflation will return with a vengeance.

Moreover, in either case, there is the threat of public debt. It is too large, and it is increasing because of the need to “print more money” to avoid the crisis with public investments.

There may come a time when the buyers of this public debt do not trust it (China and other countries are already selling part of their dollar debt, as can be seen here). If that happens across the board, we would find ourselves in a situation of default by governments, which can totally sink the value of their currency.

Given these scenarios, without having a crystal ball, my opinion is that there is a lot of risk to the stability of the euro and the dollar for the remainder of the decade.

In addition, when they tell us that we are now in a time of the “bubble of everything”, because they say that everything is at its maximum prices (the stock market, real estate, gold, …), there is a big mistake. It is not that we are in times of high value. What happens is that our meter (currency) has shrunk.

If we look at the exchange prices between goods, we have already seen the example that my house would cost less ounces of gold today than it did in 1990, so it is not at peak times.

The big problem is that what does not stand up to good comparison with the “gold coordinates”, or those of any other good, are wages. That is the cause of the transfer of wealth from those who do not have savings to those who do. It is what they call inflation theft. And it is what is generating the great social tensions. As I say, it is a big problem, but I will deal with it in future entries, since this one focuses on currencies.

What can we do?

In view of the above, and always speaking exclusively of the case of currencies, which is the one I am dealing with here, what I believe we can do to protect ourselves from the risk of the currency losing value is what I will explain below.

In the case of individuals.

- Having little of our savings “stored in currencies”. That is, little in current accounts at the bank, or in banknotes at home.

- And how much is little, because you have to have something to pay for everyday expenses.

That is true, and the answer depends on the individual. Above all, it depends on where we have “filed/invested” the rest of our savings, and how liquid that place is.

If we think that we can sell those other savings in x months, then we must have in currency something more than the expenses we foresee for x months. That amount that we will have in currency is the amount that will be at risk if a sudden currency crisis comes. But, probably, it will not be the fundamental part of our savings. - And where do we “file” the rest of our savings?

Each person must choose the place according to his activity and the world he knows best. You should choose the “unit of account” that most closely resembles the average of what is happening in your business, and seek to invest in assets that perform better than that unit of account.

In any case, in the event of serious monetary problems, it is possible that the activity of banks and governments will also be greatly affected. Therefore, investments in real assets (real estate, gold, art, …, what I call “things”) are likely to perform better. For the same reason, I do not see investing in government bonds as very advisable. As for investing in the stock market, you would have to choose companies that do not lose a lot of sales in the event of a fall in the financial world, and that this fall does not drag them down because their balance sheets are closely intertwined with those of the financial world (it will not be easy to find them). - In addition, if inflation starts to be very strong, you have to “get rid” of dollars or euros immediately after cashing them. This can be by bringing forward necessary purchases in the short term (they will be more expensive in the future), or by exchanging the currency for something very liquid (gold? bitcoin?, …).

For the case of companies.

The above applies to individuals. However, since companies have more means, they must act professionally in the following:

- They have to look in great detail for the currency they choose as the “unit of account” for their analytical accounting. Which, of course, must be closely related to their business.

- Once they have found that currency, they must make all their balances and projections in that currency. In addition to doing them in euros or dollars by legal obligation.

- In addition, they should try to have the best possible approximation of the balance sheets, in that currency, of their customers and suppliers in their production chain. Based on this information, they will be able to make decisions on which customers and suppliers to replace because their stability is at risk.

- They also have to choose the place where they will “store” their excess cash, which should not be in fiat currencies. The logical choice would be a real asset that is closely related to their business, that performs well in times of stress, and that is relatively liquid for the times when they need to use the cash.

Conclusion

The current situation of currencies, especially the dollar and the euro, presents significant challenges for both individuals and businesses. The steady loss of value, aggravated by inflation and growing economic uncertainty, calls into question the ability of fiat currencies to continue to fulfill their role as a store of value and unit of account. In this context, it is essential to rethink how we measure our wealth and look for more reliable alternatives, such as gold or other real assets, that offer greater long-term stability.

To protect ourselves from these risks, it is key to reduce our exposure to fiat currencies and diversify into tangible assets that are more resistant to currency crises. Although there is no perfect solution, adapting our decisions to the reality of each sector and activity, and considering units of account that are closer to our economic reality, can offer us greater security in an increasingly uncertain financial environment.

*****

Readings that have interested me.

In the process of writing this entry I have come across many issues of other subjects. I would like to share the following, which is closely related to the above.

The fact is that Seekingalpha, which is a highly recommended website, publishes a news item that has been little reported in the conventional media. It can be seen here. The fact is that the Fed has taken the decision to increase the capital requirements of large US banks by 9%. That is much less than the 19% that was planned, and more than the 5% that the banks expected.

I say that the news is relevant because it shows the great risk in banking. If the Fed has not dared to maintain its plan to increase it by 19%, it is because they know that, by doing so, they are putting the stability of the banks at risk. In other words, it is not true what they tell us that their balance sheets are healthy and they are very resilient. And if the banks are complaining about the 9%, it is because even that hurts them.

Also, this news fits in quite nicely with the much publicized news that Warren Buffett is selling banking stocks. It seems that they do not give him confidence.

On the other hand, it is also highly recommended to read this recent article by Ray Dalio. It provides many graphs to summarize the state of US power hegemony. The summary is that the decline is clear.

*****

As always, I welcome comments on my email: pgonzalez@ie3.org