Protection against the storm

Written by Pablo González and Pedro Nonay, trying to find what we can do in our adaptation to changes in world order.

Entry 11

The concept of money needs to be rethought.

20 June 2025

My new context selection.

Before going into the specific subject of this entry, I would like to mention an important and recent change of context in the evolution of the new world order that we are investigating in our writings since 2020. It is the aggressions between Israel and Iran. The situation is one of great danger and many repercussions, however it turns out.

As of today, all possibilities are open. They may reach a cease-fire of hostilities soon. A global nuclear war may break out. The current Iranian regime may also fall, …

Any of the alternatives entails high tension in the short term, and markets with a lot of volatility (pay attention to the rise in the price of oil, which affects the entire world economy). It is also the case that, in the medium and long term, there will be a consolidation of the division of the world into the two blocs of countries of which we have spoken so much. In other words, a move towards bipolarity. Of course, the question remains as to which bloc Iran will end up in, which is no small matter.

*****

More on currencies, with AI support.

In the previous entry 3 I wrote about currencies. I came to say that I do not consider them a good unit of measurement of our patrimony.

I didn’t say it at the time, but I was left wanting to make more comparisons to support my intuition.

I would have liked to compare the evolution of prices with something similar to barter for a long time. I wanted to look for a comparison with two very different “assets”. One of them was to represent the first necessity in low-income areas. The other was to be the opposite, something like the representation of luxury.

Without much of an analysis process to choose those assets, but with some logic, I decided that the “humble” asset could be potatoes, and the luxury asset could be Rolex watches. Both assets have been around for a long time and have not changed in their qualities, so they could be valid for comparisons.

The problem is that it was not clear to me how to obtain historical price series of these assets in a homogeneous way.

It occurred to me to ask those series to artificial intelligence, which is able to search and sort historical data in a way that I can´t so easily.

I was delighted with the results, and I want to share them here, because I think they are relevant to insist on the “uselessness” of the currency concept we have been using for a long time.

The issue is that I asked the AI (Grok, in this case) to make me a list of annual prices, from the year 2000 until today (i.e. 25 years) of the following products:

- The ounce of gold. It is clear that for this I did not need the AI, since there are many official market tables, but this allowed me to make comparisons to see the reliability of the AI list, which turned out to be quite acceptable. I should clarify that I asked for average annual prices, and that the one for 2025 is not valid because the year has not ended.

- The square meter of housing in Madrid. For this there is also a lot of data without needing the AI, but it is not so simple to homogenize them. It so happens that I know this market a little bit, so I could also check the results offered by the AI, and I also found them acceptable. These are average annual prices.

- Official inflation in Spain (IPC). Clearly, this data is accessible without the AI, but I found it faster to obtain it with its help.

- The price per kilo of potatoes. This is a market that I am hardly familiar with. The conversation with the AI led me to realize that I could not get homogeneous price data for the final consumer in supermarkets, because it is very much influenced by promotions and other issues. It was easier to look for wholesale prices. It also became clear to me that prices varied a lot by region and by potato type. After that, I decided to ask for data for wholesale sour potato in Castilla y León (producing region in Spain), in average annual prices.

- The price of the Rolex watch. In the conversation I could see, as it is known, that there are different models of Rolex watches, each with its price. I looked for one that has not changed much over time in its design (so that prices were homogeneous), and that is something massive within the luxury market (so that excessive exclusivity does not distort the price). For that reason I chose the steel Submariner model.

I also made a comparison with other IAs to see the consistency of the data. And this consistency was found, always within an order, because they are annual average prices.

After all this, I asked the same AI to give me the final price list in a single column. This allowed me to easily transfer it to an excel sheet. In addition, Microsoft’s AI support tool allowed me to generate graphs automatically based on my excel.

That is to say, with very little work I was able to generate the graphs that I present below. And many more can be made. In fact, I have explained the system so that the reader can generate the ones that seem most appropriate for his interest.

Charts and my deductions.

After what has been said above, I present the generated graphs.

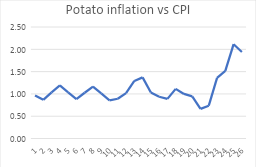

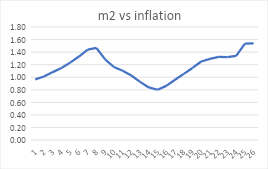

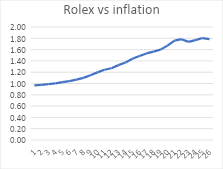

- Comparison with inflation.

It is clear that, although each of the products behaves differently, they have all undergone price increases far in excess of official inflation so far this century (between 50% and 100% higher). And it is important to realize that each of the products (potatoes, housing, and Rolex) are intended to represent very different types of consumption.

First conclusion: despite what we are told, the inflation figure is very unrepresentative of the reality affecting consumers. This is something we all sensed, but this makes it clearer.

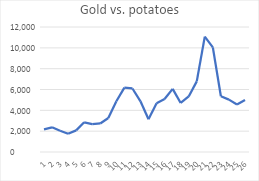

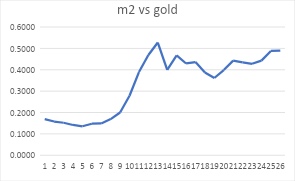

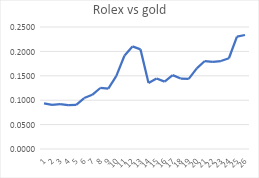

- Comparison with gold.

What the first graph below shows is that, in the year 2000, with one ounce of gold you could buy about 2,000 kilos of potatoes, and in the year 2025, about 5,000 kilos. Moreover, despite the variations over time, in almost every year you have been able to buy more kilos than in 2000 with the same amount of gold.

The second graph shows that in the year 2000, with one ounce of gold you could buy 0.17 m2 of housing, and in the year 2025 you can buy 0.49 m2 (almost three times as much). And almost every year you can buy more m2 than in 2000 with the same amount of gold.

The third graph says the same thing. With one ounce of gold in the year 2000 you could buy 0.1 Rolex, and in 2025 you can buy 0.23.

Second conclusion: despite the fact that, measured in euros, potatoes, square meters of housing, and Rolexes have had quite a lot of inflation as we have seen above, measured in gold, they have all dropped a lot in value, albeit with temporary differences in each market.

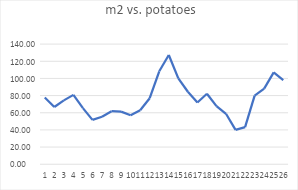

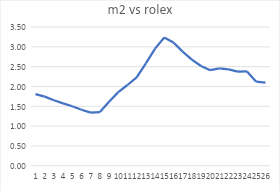

- Comparison between them (barter).

The first graph below tells us that, with 1,000 tons of potatoes, in the year 2000 you could buy 78 m2 of housing, and in 2025 you can buy 98 m2. The increase is small and, in addition, over time there have been times when you could buy a little more or a little less.

The second graph tells us that, with a Rolex, in 2000 you bought 1.81 m2, and in 2025 you buy 2.1 m2. As in the previous case, the increase is small and, in addition, over time there have been times when you could buy a little more or a little less.

Third conclusion: Both against basic goods (potatoes) and luxury goods (Rolexes), the square meter of housing has been almost stable in this quarter of a century in barter with those goods.

General conclusion.

Throughout the first quarter of this century, goods have gone up in price in euros, and down in gold. However, they have been relatively stable in exchange prices between them (barter).

That is to say:

- To exchange one good for another, we don’t care about the timing. Although, of course, if the timing is well chosen, there is some benefit.

- For savings, it is much better to have them in gold than in euros. It is also better to have them in gold than in m2, potatoes, or Rolex.

All this with the nuances that the calculations are made for Spain, so far this century, and with the possible errors of the AI data. However, the AI errors do not worry me too much, because I have made sure that the general line was correct, and because I was looking for the order of magnitude, not the detailed data. It could be that with more elaborated data it changes some decimal places, but it does not change the concept.

Summary: the currency is not valid to monitor the value of our assets. This is independent of the fact that the law obliges us to do our accounting and tax returns in that currency.

On the other hand, it could be that, in other places, or with other assets, different values come out (I do not expect this as a general rule, but there will always be exceptions). That is why I have explained the working system. Seeing how easy it is, I invite readers to apply it to the places and assets that interest them. I have done it for the ones that interest me. Of course, I also suggest that readers spend some time talking to the AI to “clean up the data”, as the first answer should not be accepted.

*****

Income from work vs. income from capital.

As we have seen above, with good planning it is possible to ensure that the value of your assets does not decrease. It is necessary to choose to have it invested in assets that do not lose value. And note that, when I say that they do not lose value, I am not talking about their value measured in fiat currencies, but in their capacity to be exchanged for other assets.

The big problem appears when we talk about the income from work. I am referring to the majority of the population, whose income depends on “selling their working hours“.

It happens that whoever sells their working hours for a living, usually gets paid for those hours in fiat currency, based on the contract they have. And those contracts are usually indexed to the CPI for annual increase negotiations.

The fact is that it has become clear that fiat currencies are losing value in terms of their exchangeability for other goods. And that the CPI is designed (manipulated) not to reflect all that loss of value.

This means that those who are paid in fiat currencies will be able to buy less and less of anything (potatoes, housing, Rolex, or whatever) every year.

In other words, we face a situation of “wealth transfer”. Those who already have wealth can defend their ability to exchange it for other goods quite well. And those who do not have it, and live on their wages, are guaranteed to lose purchasing power.

This is what we hear so much about, that the system is encouraging the rich to get richer and the poor to get poorer. It is not automatic (there are always exceptions), but it is most likely.

This leads us to a major problem of “social contract”. In principle, the system we have lived through during the twentieth century (it was not quite like that before), rewarded personal effort. With work, and with intelligence, it was possible to belong to the social class of “those who have”. Now it seems that we are returning to the old system: work does not allow one to move up the social ladder, it even guarantees one’s descent.

I see it as logical that there should be incentives for “the haves”. Their investments generate jobs, and their patrimony was earned with effort, so they deserve respect and to be able to enjoy what they earned. But, it is not so logical to block the way for those who do not have patrimony today, but do have intelligence and effort.

If we continue along this path, we will end up with a society of “rich fools”, because they stopped studying and making an effort, since it was easy for them to live well by doing little; and of “smart and bitter poor”, because their efforts do not bear fruit. This is a guarantee of social conflict.

It is necessary to find a way to put the social elevator back into operation. To do so, it would be necessary to abandon the system of paying salaries in fiat currency (even if it is indexed to this manipulated CPI). A difficult issue.

In short, although it may not be noticed, it is the evolution of the currency that is generating all the problems. And we must correct that trend.

*****

Currency and international trade.

I have already said above that currency (the way we manage it) is the cause of the problems of social conflict in every country. We all calculate mentally in those currencies, but they do not work well for the management of our wealth, nor for the remuneration of work.

The fact is that currency is also the cause of conflicts between countries. We are seeing it today with the debates about the reliability of the dollar, and with the consequences of protectionist measures, such as tariffs.

It is well known that, since Bretton Woods, the USD has been the reference currency for international contracts. It is also well known that investing in U.S. debt was unprofitable, but very safe in terms of protecting value. But that is in big flux. In fact, Moody’s has very recently downgraded US debt, which is serious (news here, and in a thousand places the reader will have seen).

After the division of the world into two blocs of countries (which is what is happening now), the BRICS bloc is losing confidence in the USD for its contracts and in US debt for its investments. And, because of this fear of BRICS money moving away from the USD and US bonds, it happens that money from the West is also afraid that these assets will lose value.

The new currencies have not yet been generated, but we are in the process. An example is what the BRICS bloc is trying to do with the mBridge system (see here). They are looking for a system to organize their international contracts without using the USD, and without needing the SWIFT system (which they have become afraid of after what was done with the sanctions against Russia for the war). It’s something that doesn’t work well yet, but it draws the line.

Meanwhile, international markets are experimenting with so-called “stablecoins”, which are cryptocurrencies theoretically supported by other fiat currencies. This is a more important issue than it seems. That is so because if, for example, a USD-backed stablecoin succeeds (as is the case of the so-called USDT), according to the theory of those currencies the issuer has to have as many fiat currencies backing as cryptocurrencies issued (another thing is that they comply with it, but that is the theory). That is, a successful use of tether (which is the other name for USDT), implies demand for USD, so it would not lose so much value. Maybe that is why, and because of the geopolitical war, in Europe they are prohibiting (or inconveniencing) the use of Tether.

My personal opinion about those stablecoins is bad. But my opinion doesn’t matter. What matters is what the markets actually do. If we believe that conventional fiat currencies are at risk (I do), I would see it better to focus on non-fiat backed cryptocurrencies (such as Bitcoin may be). In that case, if you don’t trust the holding of Bitcoin, just buy it 10 minutes before you have to make the payment, and the receiver sells it 10 minutes after receiving the payment.

In general, work is being done to dethrone the dollar as the base currency for international trade, but this will not happen quickly, due to the lack of alternatives. We are not facing a risk of a sudden fall of the dollar, but a risk of a gradual loss of strength (explained well here).

The famous tariffs.

Within this international trade issue, Trump’s actions with tariffs (constantly one step forward and one step back) are all the rage.

The fact is that many arguments can be used to discuss whether or not these tariffs are necessary. One can talk about free trade, or the need to balance trade balances, or … But what is not usually verbalized much (although it is in the minds of all actors) is that the law of a country works within that country. And, if international trade ends up representing a significant percentage of a country’s GDP, there is going to be a significant percentage of the economy over which the country can impose its law with difficulty. That is what the tariff issue is trying to fix (more or less successfully).

The result is that either the size of the country is increased, so that what used to be “exports-imports” are now “domestic trade” subject to the same laws, or a way is sought to reduce these exports-imports.

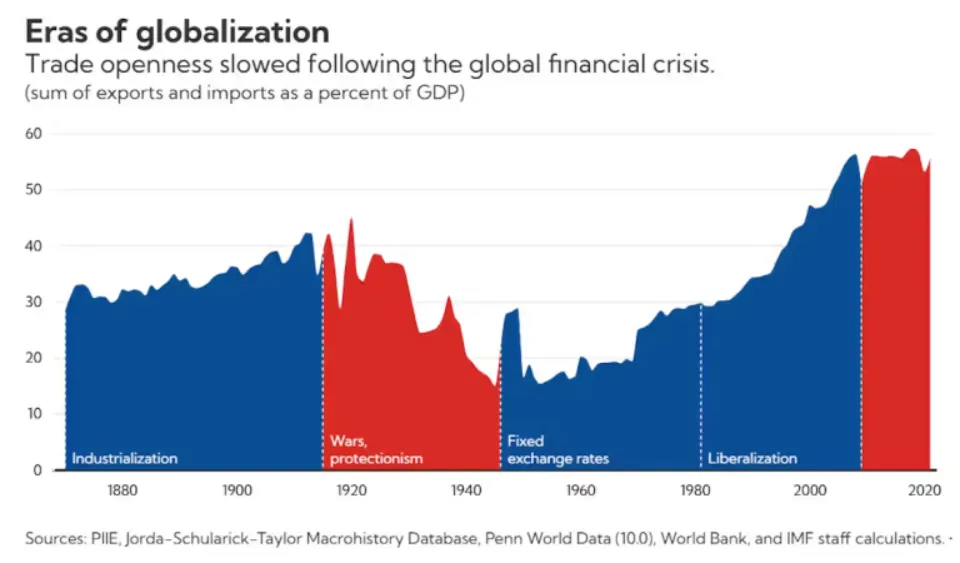

The following graph is interesting:

It is clear that we are at a time when international transactions represent the largest percentage in recent history. And that is something that states cannot bear. The normal thing to do is to reduce these markets, with tariffs or other instruments. If they don’t, states lose control of their economy.

The other alternative is the one also proposed by Trump. That of making his country larger in size, with the annexation of territories with which it has a lot of trade now considered international.

A different approach.

In the face of all the above problems of the functioning of the currency as an instrument to manage the growth of society, there are proposals with a radically different approach. They do not seek to find a new currency that works better. What they seek is to take power away from the concept of “currency” and from the concept of “capital”. This is what Albert Wenger does in his interesting book (here). What he is saying is that the technological revolution in which we find ourselves has the same consequences for the change of societies as the invention of agriculture, or the industrial revolution (I agree with him on this).

He says that the importance of capital in the society that is now ending has its cause in that it was necessary to maintain the capitalist system (the name itself gives some clue). Just as it happened before, in the fundamentally agricultural epoch, in which the important thing was the possession of land.

His thesis is that in the revolution we are facing, the important thing is knowledge, and getting attention to transmit it. And that can be done without much capital.

I think he is fundamentally right. And that this will be the case in the long term. I also believe that there is still a short period of time in which capital will continue to be important, and it will be important to choose the currency that represents it. However, it is representative of the importance of what he calls “attention” the growing strength and remuneration of influencers, who have built their profile without the need for capital.

*****

As always, I welcome comments on my email: pgonzalez@ie3.org