Building the new order

Written by Pablo González and Pedro Nonay, trying to know how the new world will be.

Entry 16

International agricultural flows (II).

21 March 2024

You already know that I try to make each entry independent of the previous one, but that I have a common thread: I seek to deduce how the new world order is going to be organized after everything that is happening.

My new context selection.

I usually begin my entries with this “new context” heading in which I summarize the most relevant of what has happened since the previous entry regarding the evolution of the new order. My selection today is as follows:

- Putin has granted an “interview” to Tucker Carlson on February 9. It can be seen here, although I warn that it lasts two hours. I put the quotation marks because, in my opinion, rather than an interview, this is a lecture by Putin aimed at listeners in the West. The answers are twenty minutes long, and the interviewer does not direct anything. Putin comes to say that he has his historical reasons for deciding to go to war (normal for him to say so). He also says that the economy of the West is in trouble, while the strength of the BRICs+ is outstripping that of the G7. In other words, he sends the message that it is time for them to give up and accept reality, … or it will be worse for the West.

- On February 16, Russia announced that the opposition leader and prisoner Navalni has died in prison. Everywhere (except in Russia) there is talk of murder. It remains to be seen whether this will have an effect on Russian public opinion. For now it does not seem to.

- On the other hand, Putin has signed a decree allowing Russia to confiscate energy assets in Russia from companies of enemy countries (news here).

*****

Analysis by product.

Following the previous entry, I will now look at each product independently.

I am doing so in the search for possible countries to “sign” to ensure that the Western bloc has its food supply solved.

However, it should be noted that the data I am going to work with are current (or not very old), while future developments may give different results. This may occur because more land is put into exploitation, the current land is sown with different grains, there are significant natural disasters, geopolitics change the destination of exports, there are technological innovations that improve yields, … That is, everything can change a lot in the future, but at least we must have a “snapshot” of the current situation.

A very visual way to prove that everything can change a lot (and has always changed), can be seen in this interesting animated graphic.

It is also interesting to recall that the management of international agricultural flows has already had an impact on geopolitics and economics in the past. A relatively recent example is what was called the “Great grain robbery“. It happened in 1972, when the Soviet Union needed to buy grain from the USA because of its droughts. The fact is that agriculture was subsidized in the USA, so the Russians were able to buy cheaply. Because there was greater demand (Russian), prices rose in the USA, which generated social and economic problems there. In other words, the USA had “subsidized” the Soviet Union (news here). In addition, there is a legend that the multinationals in the sector made huge profits by taking buying positions before informing the market of the sales to the Soviets.

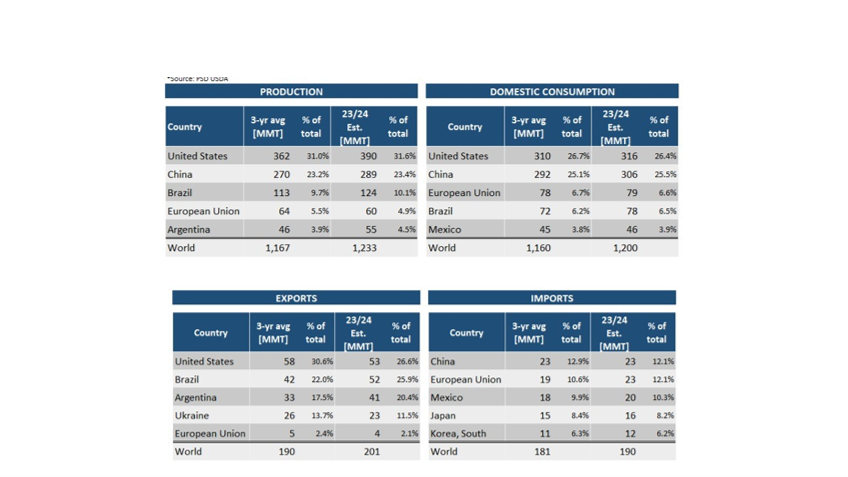

Corn.

Regarding the uses of corn, it is important to know that only 10% is used for human consumption. The rest is used, almost equally, in animal feed and ethanol production (source: Ceres).

With the help of Pedro and Eloy Perez (thank you), I have obtained the following data concerning corn. They show the main producing, consuming, exporting, and importing countries, ordered from highest to lowest.

I work with these data based on the column of the average of the last 3 harvests, since the averages avoid (somewhat) that the data are contaminated by punctual events. Based on these data it can be deduced that:

BRICS+ bloc:

- China produces 270 MMT, and consumes 292 MMT, so it is in deficit (although these are not large deficit percentages, they are very important figures for the international flow).

For that reason, it is forced to import 23 MMT, being the largest importer. As we will see later, if China does not want to depend on the USA, it needs Brazil. In addition, China also imports from Ukraine, an issue that will have to be seen if it changes after the war. - Brazil produces 113 MM and consumes 72 MMT, so it is clearly in surplus. It exports 42 MMT.

Brazil, a member of the BRICS+ bloc, is perfectly capable of making up for China’s deficit. And it has enough to export to other deficit countries of the same bloc.

Western Block:

- The USA is in surplus, exporting 58 MMT.

- The European Union is in deficit, importing 19 MMT, although it also exports 5 MMT, so its deficit is 14 MMT.

Here it is worth mentioning that, although the EU appears in the table as one country, for the purposes of grain there are several EUs. In the south and north it is in deficit, but in the center it has some surplus. Therefore, there are flows within Europe. - The other major importing countries of the Western bloc (Mexico, Japan, and South Korea) import a total of 44 MMT.

- If these countries only traded with each other, the accounts would be balanced, but very tight.

- In addition, Argentina (which can now be considered as part of the Western bloc, although the evolution of its contracts remains to be seen) has a large surplus, exporting 33 MMT. These quantities could be used to make up for the deficits of the other western countries, which do not appear in the table because they need to import small quantities each.

- We will also have to see how the Ukraine War ends and how its export capacity of 26 MMT is divided among blocks.

Therefore, in the big numbers it seems that both blocks of countries would be almost balanced in terms of their capacity to have the corn they need. That is on the condition that Argentina is confirmed to be in the western bloc, and with the future of Ukraine in doubt.

However, the different elasticities of demand must be taken into account. When the demand is for food, it is very inelastic (e.g. Mexico, which needs corn for pancakes, with no possible substitute). It is not so inelastic when the demand is for biofuels or animal feed.

In any case, the seasonal variation of harvests in each country must be taken into account. It will surely happen that when a country needs to import, the country that is supposed to supply it has not harvested yet. That will be something to be solved by traders (and by some trading between blocks).

Wheat.

It is important to know that wheat is responsible for 20% of the calories consumed by the human population, mostly in the form of bread, pasta, cookies, … 65% of wheat production is used for this purpose. In addition, 17% is used for animal feed.

With the help of Pedro, and Eloy Perez (thank you), I have obtained the following data concerning wheat.

As in the previous case, I work with these data based on the column of the average of the last 3 harvests. Based on these data it can be deduced that:

BRICS+ bloc:

- China produces 136 MMT, and consumes 150 MMT, so it is in deficit. For that reason, it is forced to import 11 MMT, which may not seem to balance the numbers, but it does considering what it had in storage.

- India produces and consumes 107 MMT, so it is balanced.

- Russia produces 84 MMT, and consumes 42 MMT, so it has a large surplus. For that reason, it exports 40 MMT. In addition, Pedro says that Russia’s wheat production is increasing a lot, which will allow it to export more.

- Egypt imports 12 MMT, Indonesia 10 MMT, and Algeria 8 MMT, totaling 30 MMT.

Then, the main countries of the BRICs+ bloc import 41 MMT, and Russia exports 40 MMT.

It might seem that there is balance, but the smaller countries in the bloc also need to import something. In other words, it seems that the BRICS+ bloc is not perfect in this. Much less so if it ends up turning out that Turkey will go for that bloc, which is doubtful, given that its current position is a bit ambiguous.

Western Block:

- The EU produces 133 MMT, and consumes 107 MMT, so it has a surplus of 26 MMT.

- The USA produces 46 MMT, and consumes 30 MMT, so it has a surplus of 16 MMT.

- Australia is also in surplus, exporting 28 MMT. Canada is also in surplus, exporting 22 MMT.

Therefore, it seems that, as far as wheat is concerned, the western bloc is in surplus. Although it must be considered that the smaller countries of this bloc may need support.

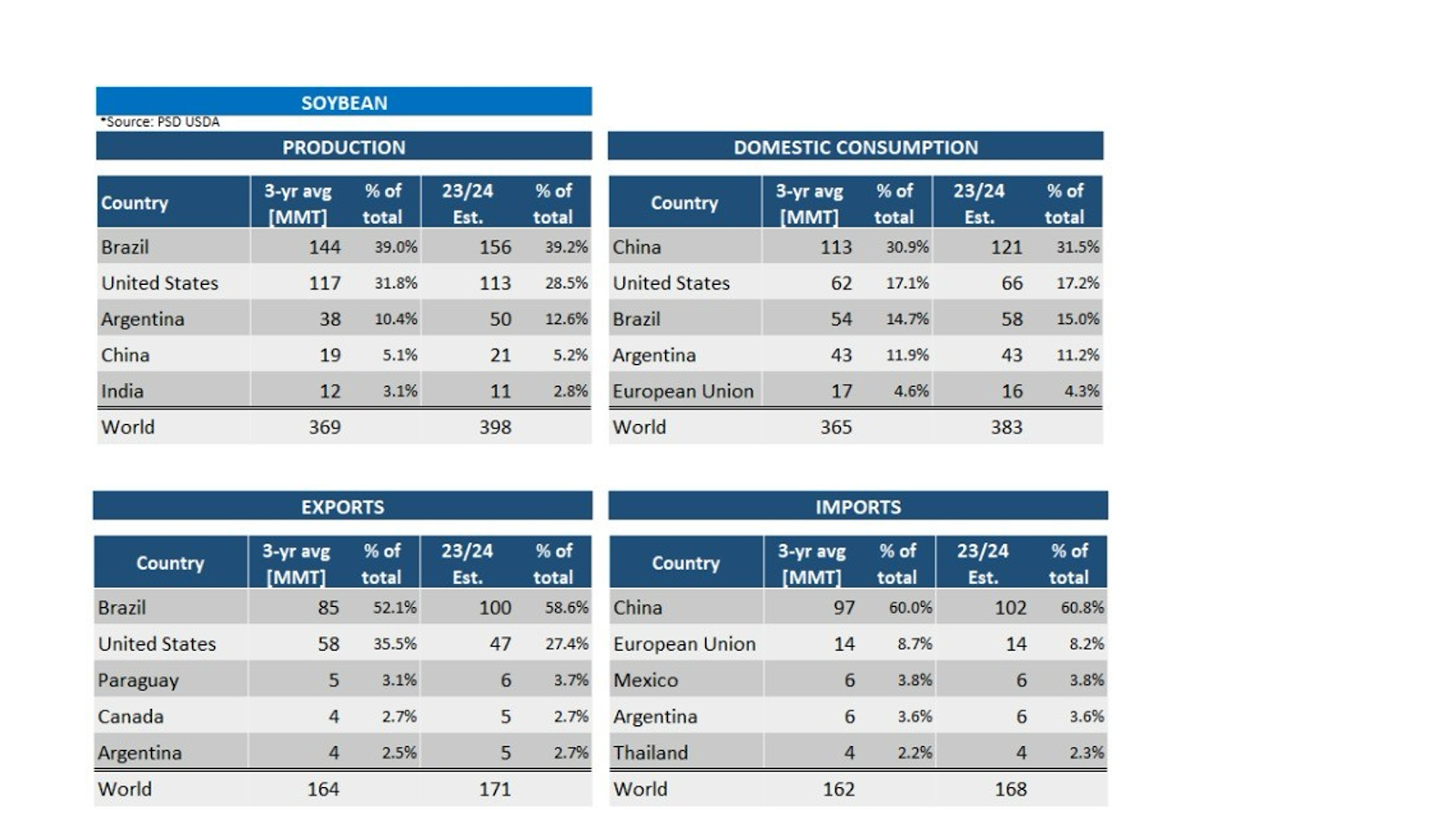

Soy beans.

Before analyzing, it is important to know that the main use of soybeans (67%, according to Ceres) is for animal feed, and 17% is for vegetable oil, which is used for cooking and processed foods such as margarine. In other words, its effect on human food is mainly due to its capacity to “produce meat” through animal feed. On the other hand, a significant amount of soybean production in the USA is used to make biofuels, an issue that could be debated more than it is.

With the help of Pedro, and Eloy Perez (thank you), I have obtained the following data concerning soybeans.

As in the previous cases, I work with these data based on the column of the average of the last 3 harvests. Based on these data it can be deduced that:

BRICS+ bloc:

- Brazil produces 144 MMT, and consumes 54 MMT, so it has a large surplus. For this reason, it exports 85 MMT (which does not add up to an exact balance, due to differences in storage).

- China produces 19 MMT, and consumes 113 MMT, so it has a large deficit. For this reason, it is forced to import 97 MMT.

- India produces 12 MMT, and is neither among the major consumers nor among the major importers, so it appears to be in surplus (or in a short deficit).

- Thailand is an importer for 4 MMT. Paraguay is an exporter for 5 MMT, although it is not very clear which block it belongs to.

As the smaller countries in the bloc will also need some soybeans, it appears that the BRICS+ bloc is in deficit in soybeans by quantities that may exceed 17 MMT.

Western Block:

- USA produces 117 MMT, and consumes 62 MMT. Then it is very surplus, and exports 58 MMT (as always, the difference must be the change in warehouses).

- Argentina produces 38 MMT, and consumes 43 MMT, so it is in deficit, and imports 6 MMT, but exports 4 MMT (which must be caused by the difference in warehouses and harvest times).

- The European Union is not a significant producer, and consumes 17 MMT, and imports 14 MMT, so it is in deficit.

- Canada is in surplus, exporting 4 MMT.

- Mexico is in deficit, and imports 6 MMT.

Then, as for the large countries, the Western bloc has a surplus of about 40 MMT of soybeans. It can devote them to the needs of the small countries of its bloc, or to negotiate with the BRICS+ bloc.

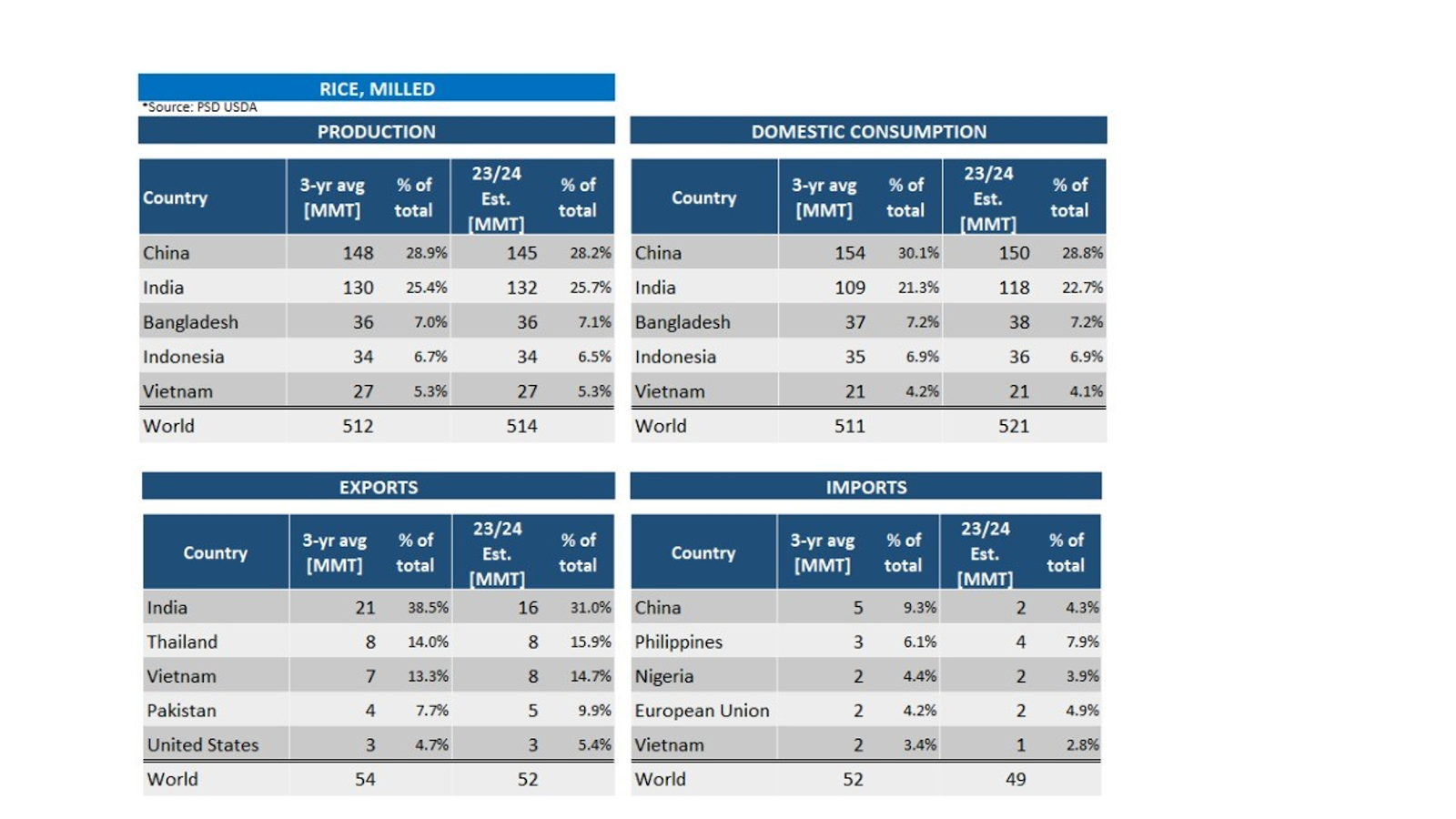

Rice.

With the help of Pedro, and Eloy Perez (thank you), I have obtained the following data concerning rice.

As in the previous cases, I work with these data based on the column of the average of the last 3 harvests. Based on these data it can be deduced that:

BRICS+ bloc:

- China produces 148 MMT, and consumes 154 MMT, so it is in deficit (although not in large percentages). For that reason, it is forced to import 5 MMT (again, the lack of balance of the figures will be a difference of warehouses).

- India produces 130 MMT and consumes 109 MMT, so it has a surplus. It exports 21 MMT.

- Bangladesh produces 36 MMT, and consumes 37 MMT, so it is very balanced. The same happens to Indonesia, which produces 34 MMT, and consumes 35 MMT.

- Vietnam produces 27 MMT, and consumes 21 MMT, so it is in surplus and can solve the small deficits of other smaller countries in the block, exporting 7 MMT, together with Thailand, which exports 8 MMT, and Pakistan, which exports 4 MMT.

- The Philippines needs to import 3 MMT, and Nigeria 2 MMT.

Then, it seems that, with respect to rice, in the large countries of the BRICS+ bloc, there is a surplus of 28 MMT, which may be sufficient for the needs of the smaller countries of the bloc.

Western Block:

- As for rice, no country in the Western bloc appears as a major producer or consumer. Only the USA appears as a small exporter, with 3 MMT, and the EU as a small importer, with 2 MMT.

Then, it seems that rice is not a major problem in the western bloc, unless the addition of small deficits in many small countries of the bloc would complicate the result.

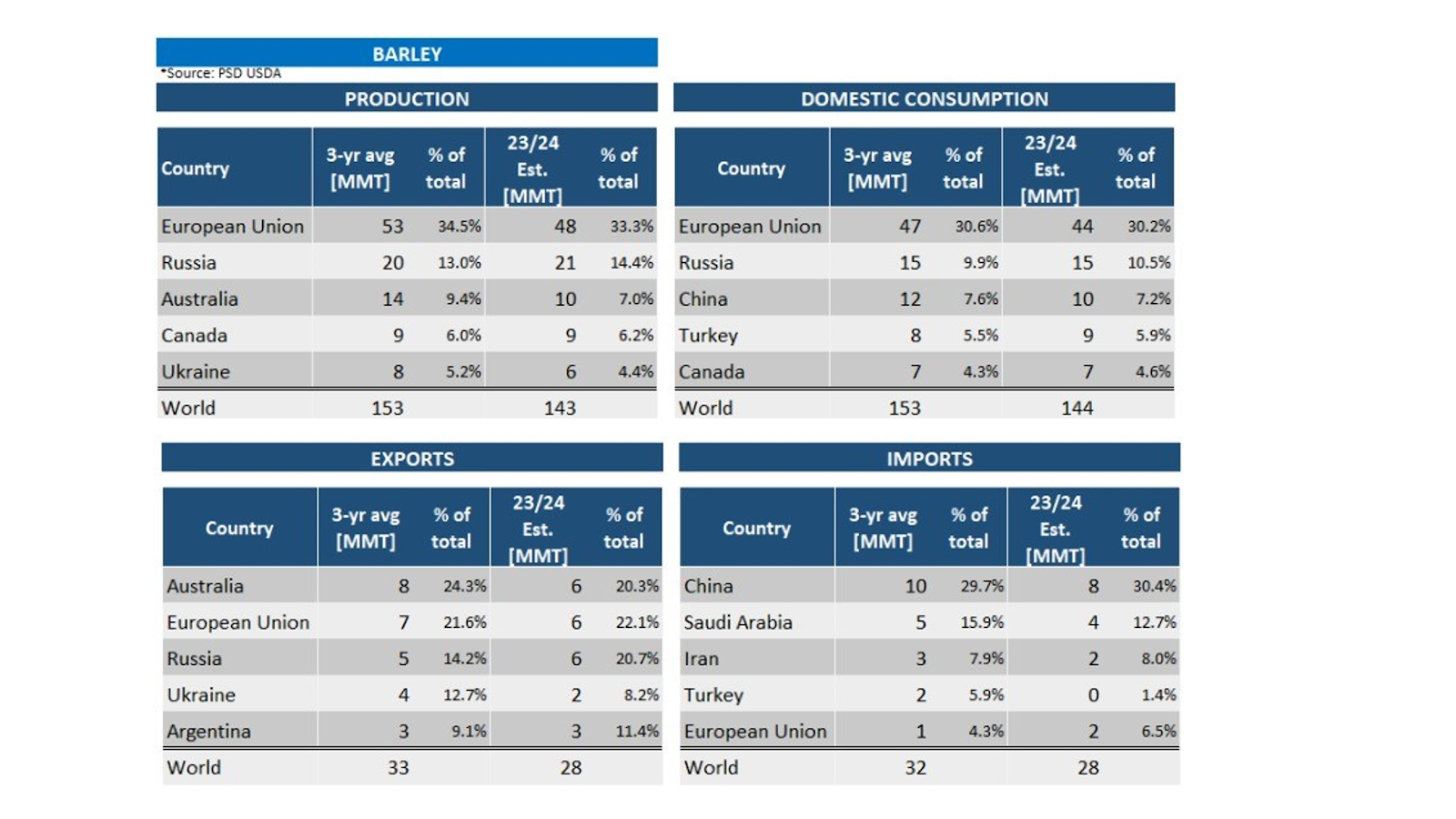

Barley.

With the help of Pedro, and Eloy Perez (thank you), I have obtained the following data concerning barley.

As in the previous cases, I work with these data based on the column of the average of the last 3 harvests. Based on these data it can be deduced that:

BRICS+ bloc:

- Russia produces 20 MMT, and consumes 15 MMT, so it has a surplus. For this reason, it exports 5 MMT.

- China is not a major producer, and consumes 12 MMT. Therefore, it is forced to be the largest importer by 10 MMT. The same is true for Saudi Arabia, which imports 5 MMT, and Iran, which imports 3 MMT.

- It is not clear in which block of countries will remain the part of Ukraine that is the largest barley producer. In any case, Ukraine produces 8 MMT, and exports 4 MMT (data that must be put under suspicion, because they are the average of the last 3 harvests, and must be highly influenced by the War).

- Doubts should also be raised about Turkey’s ascription block, which imports 2 MMT.

In view of what is happening with the major countries of the BRICS+ bloc, it is clear that, even if all of Ukraine’s barley production were to remain in that bloc, there is a shortfall of about 10 MMT. And that is not counting the sum of what is needed by the smaller countries of that bloc.

Western Block:

- The EU produces 53 MMT, and consumes 47 MMT, so it has a surplus, and exports 7 MMT, although it also imports 1 MMT (due to warehousing and harvesting times).

- Australia produces 14 MMT. It is in surplus, and exports 8 MMT.

- Argentina has a surplus and exports 3 MMT.

Then, with respect to the large countries of the Western bloc, it appears that there are barley surpluses of about 17 MMT. Even if some of that is consumed by the smaller countries of the bloc, it seems clear that the rest will be destined to cover the shortages of the BRICS+ bloc.

Conclusions.

After the study done above, I repeat that the details not analyzed can change the picture a lot, as can future crop developments, new land devoted to cultivation, or geopolitical decisions about which country joins which bloc.

In any case, in this photograph, it seems that the result is:

- Regarding corn, there is almost a balance between the blocs. But it is very clear that China depends on Brazil.

- In wheat, the West is in surplus, and the BRICS+ bloc is “tight”.

- For soybeans, BRICS+ is clearly in deficit, and the West is in surplus. China depends on Brazil, and Brazil needs China as a customer.

- In rice, it seems that none of the blocks have relevant problems.

- For barley, BRICS+ is very much in deficit, and the West is in surplus. This is said in percentages of demand, since, in terms of volume of flows, barley is small compared to other grains.

In other words, in a larger summary, the West has few problems with food grains, and the BRICS+ bloc is worse off.

This leads us to think that the West should use this “competitive advantage” to negotiate its problems in other areas, such as energy or raw materials. Especially taking into account that food, although it does not represent large economic figures in comparison with world export flows, does represent the peace of society avoiding famine (and no ruler wants a hungry population).

By the same token, the West should do everything in its power to prevent the BRICS+ bloc from recruiting for its “alignment” any country that would help it solve the problem. In that sense, it occurs to me that it may already be doing so, and that Argentina’s recent renunciation to join that bloc may be caused in that reason.

In fact, if we consider the BRICS+ bloc without Argentina and without Ukraine, we find that supply is controlled by Brazil and Russia, and demand is controlled by China. And that means great bargaining power for those who control the supply. And, since there is little doubt that Russia is part of the bloc, it turns out that Brazil becomes a “game changer”, since its hypothetical change of side destroys all balances.

On the other hand, I am told that 75% of Ukraine’s production is generated in the west of the Dniepper River, which is the part that seems to be attached to the Western bloc. In other words, the BRICS+ bloc cannot count on it.

Pedro uses an acronym to define the situation. He calls it BAU (Brazil, Argentina and Ukraine). He says that the three countries are “game changers”, that their change of sides would change the whole situation. He calls them “equidistant” countries. He says that, whichever bloc they belong to, they will assert their strength by threatening their bloc with change, for which they will try to have some trade door open with the other bloc.

Another aspect to be taken into account is that the European Union, seen in isolation, is in a bad situation. In general, it is in deficit. Moreover, climate change is making it worse off. And the CAP is not fulfilling its theoretical objective of providing incentives for solutions. Rather, the CAP can be seen as a disease that is metastasizing in Europe. Certainly, farmers’ revolts everywhere indicate something of the sort.

Final summary.

The schematic summary of the situation (with the risks involved in simplification) may be:

- The West is doing well on agricultural issues. BRICS+ is not.

- Keeping an eye on the BAU (Brazil, Argentina and Ukraine) “lineup” is essential.

- The EU, in isolation, is in a weak position.

And these things influence geopolitics, because they affect food, which is something small in terms of the economic amounts it moves, compared to world exports, but basic to avoid famines and rebellions of the population.

As a clarification for the matter of being attentive to the BAU positions (Brazil Argentina and Ukraine), the following comments can be made:

- If Brazil, which today is in BRICS+, moves to the West, the latter would be left as a very surplus (with the problem of placing its surpluses), and BRICS+ would be left as a very deficit. On the contrary, if Brazil remains in BRICS+, this bloc remains somewhat in deficit.

- If Argentina joins BRICS+, that bloc would be balanced. Today it is in the West, and that bloc is in surplus.

- If Ukraine joins BRICS+, this bloc would be left with a surplus. The truth is that, today, Ukraine exports practically half to each bloc, which makes it the most “equidistant” country. It remains to be seen what will happen after the war, as it seems that the country will be divided, with one part remaining in Russia, and the other as a smaller Ukraine. Everything will depend on the harvests in each of the two parts of today’s Ukraine.

Of course, if we go into detail, there are variations in the situation for each product. Moreover, it is important to know that, as of today, these three countries are acting as “equidistant”, since they export to both blocs. In any case, trying to see the situation as a whole, it can be schematized as follows:

*****

Readings that have interested me.

In the process of writing this entry I have come across many issues of other subjects. I would like to share the following:

- The, unknown in the West, Chinese bank called Zhongzhi is in trouble for real estate causes. It is something to keep an eye on regarding the stability of the Chinese economy (news here).

- There is research that can solve the problem of the lack of lithium for batteries (especially in the West). The idea is to replace it with sodium (news here). They need to improve a little, but it is good news.

- Another very interesting European project is working on what they call “solar paint”. The idea is based on using nanotechnology to mimic photosynthesis and generate a more efficient substitute for solar panels (news here). It’s all very incipient, but I really like the line of work. Of course, imitating nature is the way to go, because she has tried almost everything and has reached the best results by the famous “natural selection”.

- Another potential good news is that of “geological hydrogen”. It seems that there are pockets of hydrogen in the subsoil (as there are pockets of gas). If we manage to extract it, it would be very different from what happens today with hydrogen (which we “manufacture” with water and energy). Then, hydrogen would cease to be “storage” of energy to become a “source” (news here).

- It is already a fact that AI can “learn by itself”. This will become more and more unstoppable (news here).

- I really enjoyed this dense and ironic article, where they make an analysis of almost everything that is happening in world geopolitics. The West does not come out well.

- In this other article they make an analysis of what they understand as the fall of our civilization. They put the cause in the depletion of resources. The approach is quite sobering.

*****

That’s as far as I’ll go for today.

As always, I welcome comments on my email: pgonzalez@ie3.org